According to the American Land Title Association (ALTA), on March 19, 2026, “a significant legal development has impacted the Financial Crimes Enforcement Network (FinCEN) Residential Real Estate Rule, which went into effect on March 1, 2026. Yesterday (March 19, 2026), a judge in the Eastern District of Texas issued a ruling vacating the FinCEN Residential Real Estate Rule in its entirety. In the ruling, the court found that FinCEN exceeded its statutory authority under the Bank Secrecy Act and ordered the rule be set aside. This is inconsistent with theU.S. District Court for the Middle District of Florida, which last month issued a decision in Fidelity National Financial v. Bessent. As a result, there is considerable uncertainty regarding the immediate and long-term impact of this ruling. An appeal of the Texas decision is likely, and in similar cases, it has been common for courts to stay their ruling while an appeal works its way through the judicial system.”

_______________________

by Tracey Barrett, Associate Broker

March/April 2025

Beginning March 1, 2026, a new federal anti-money laundering rule issued by the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) significantly changed reporting requirements for certain residential real estate transactions across the United States. The rule — formally known as FinCEN’s Residential Real Estate Reporting Rule (RRE Rule) — is designed to increase transparency and curb the use of anonymous entities and trusts in high-risk real estate transactions.

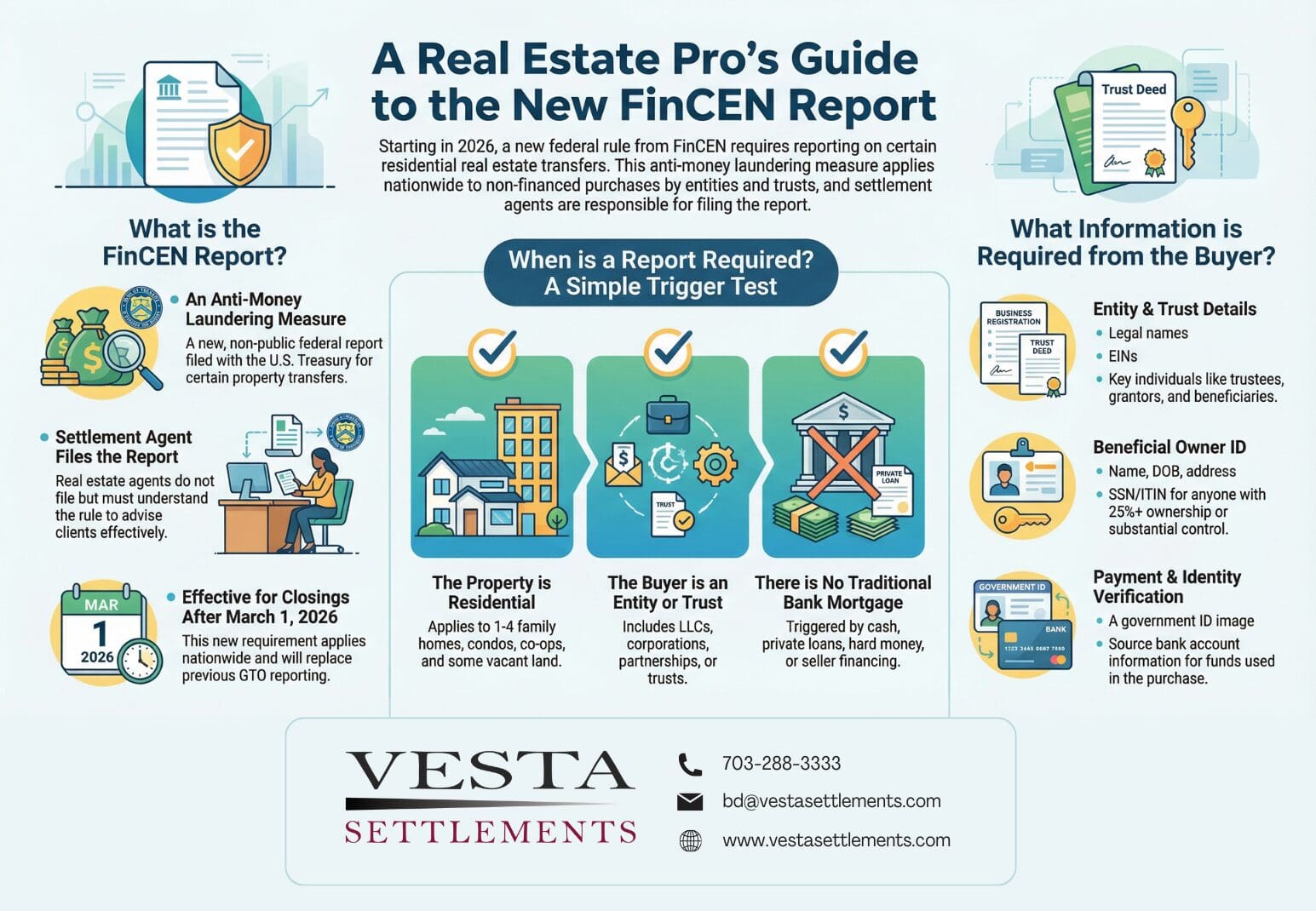

Graphic provided by VESTA Settlements

What This Means for Real Estate Investors If you purchase residential real estate through an LLC or trust, this new FinCEN rule is especially relevant to you. Starting March 1, 2026, many transactions that were previously routine for investors will trigger federal reporting — particularly those involving all-cash purchases or private financing. While the rule does not prohibit entity or trust ownership, it eliminates anonymity in these transactions.

Key Impacts for Investors:

All-cash does not mean “no reporting.” Cash purchases, seller financing, hard-money loans, and private loans can all trigger a FinCEN report if the buyer is an entity or trust.

Beneficial ownership will be disclosed. Individuals with 25% or more ownership or substantial control over the entity or trust must provide identifying information, including government-issued ID.

Gifted or no-cost transfers may still be reportable. Transfers of residential property into an LLC or trust — even without money changing hands — can still fall under the rule.

Expect more documentation before closing. Settlement providers will request ownership details earlier in the process to avoid delays. Missing information can slow or jeopardize closing timelines.

Privacy strategies should be reviewed early. If privacy or asset protection is a priority, investors should speak with legal and tax professionals before going under contract to understand compliant structuring options.

Bottom Line for Investors The new FinCEN rule doesn’t stop investors from using entities or trusts — but it does require transparency. Planning ahead and understanding the trigger conditions will help ensure smoother closings and fewer surprises once the rule takes effect.

What Is the FinCEN Residential Real Estate Reporting Rule? The RRE Rule requires a non-public federal report to be filed with FinCEN for certain residential real estate transfers that meet specific criteria. The goal is to prevent money laundering and other illicit financial activity by identifying the real individuals behind legal entities and trusts purchasing property.

This rule replaces FinCEN’s prior Geographic Targeting Orders (GTOs), which applied only in select metropolitan areas. Unlike the GTOs, the new rule is permanent and nationwide. FinCEN originally finalized the rule in August 2024 and delayed enforcement to March 1, 2026 to allow the real estate and settlement industries time to prepare.

When Is a FinCEN Report Required? A FinCEN Real Estate Report is required only when all three of the following conditions are met:

The Property Is Residential – The rule applies to residential real property, including:

One-to-four family homes

Condominiums and co-ops

Townhomes

Certain residential vacant land

The Buyer Is an Entity or a Trust – The purchaser must be a legal entity or trust, such as:

LLCs

Corporations

Partnerships

Revocable or irrevocable trusts

*Purchases by individuals in their personal name are not reportable under this rule.

There Is No Traditional Bank Mortgage – The transaction must be non-financed by a traditional bank. This includes:

All-cash purchases

Private loans

Seller financing

Hard-money loans

Even transactions where funds come from a private lender or affiliate — rather than a regulated financial institution — may trigger reporting.

Simple trigger test: Residential property + Entity or trust buyer + No traditional bank mortgage = Report required

Who Is Responsible for Filing the Report? Real estate agents do not file the FinCEN report. Instead, the obligation falls on the “reporting person”, typically the party responsible for preparing or handling the settlement or closing. This may include:

Settlement or closing agents

Title companies

Real estate attorneys

FinCEN established a reporting cascade, meaning if multiple parties are involved, responsibility defaults to the party highest on FinCEN’s priority list unless the parties formally agree in writing who will file. Reports are submitted through FinCEN’s BSA E-Filing System.

What Information Must Be Reported? For a reportable transaction, the reporting person must collect and submit detailed information, including:

Legal name and contact details of the reporting person

Property address and transaction details

Purchase price or value of the transfer

Payment method and source of funds

Information about the buying entity or trust

Beneficial owner details for individuals with:

25% or more ownership interest, or

Substantial control over the entity or trust

Beneficial owner information includes full legal name, date of birth, address, tax identification number, and a copy of a government-issued ID.

Filing Deadlines The FinCEN Real Estate Report must be filed by the later of:

30 calendar days after closing, or

The last day of the month following the month of closing

This generally gives settlement providers 30–60 days after closing to comply.

Why This Rule Matters For years, federal regulators identified real estate — particularly all-cash entity purchases — as a vulnerability in the U.S. anti-money laundering framework. Without traditional bank financing, many transactions occurred without meaningful identity verification.This rule closes that gap by requiring transparency into who ultimately owns or controls property purchased through entities and trusts. While it does not prohibit these transactions, it does eliminate anonymity. For buyers using LLCs or trusts, the key takeaway is preparation: expect enhanced identity and documentation requests well before closing.

What Buyers, Sellers, and Agents Should Do Now

Entity and trust buyers should be prepared to disclose beneficial ownership information

Settlement and title providers should update intake and compliance procedures

Real estate professionals should understand the trigger conditions to properly advise clients

Buyers seeking anonymity should consult legal counsel early to understand the implications

Final Thoughts The FinCEN Residential Real Estate Reporting Rule marks a major shift toward transparency in U.S. residential real estate. While most traditional owner-occupied purchases will not be affected, investors and trust buyers using non-bank financing should expect new compliance requirements starting March 1, 2026. Understanding the rule now helps avoid closing delays later.

2 Comments.

Really solid, dependable content. The site continues to be far more useful than average.

Thanks so much for the compliment! Like us on FB or Instagram for updates!